Budapest, 29 May 2026

Naphtha gave Asian petrochemicals a headline relief signal.

That signal is easy to overread.

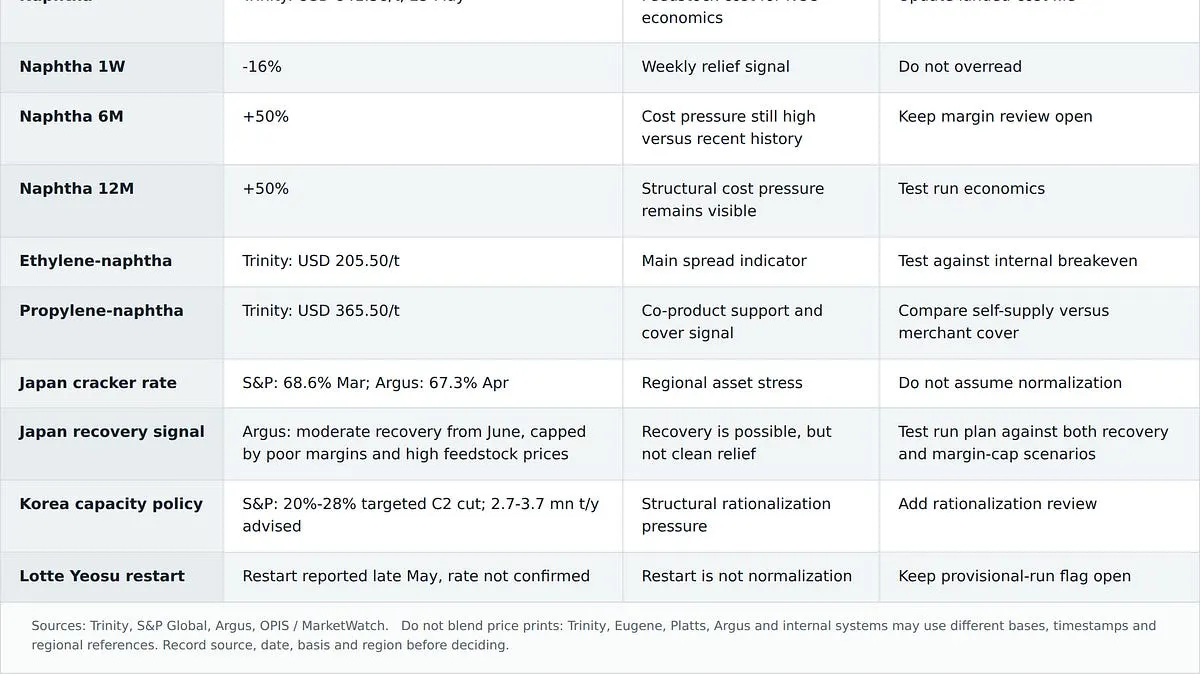

Trinity's 19-25 May commodity weekly showed naphtha at USD 841.38/t on 25 May, down 16% over one week, but still up 50% over six months and 50% over 12 months. The same table put ethylene-naphtha at USD 205.50/t and propylene-naphtha at USD 365.50/t.

That is not clean relief.

It is a stressed chain easing off emergency highs.

The price print is not the operating decision

A cracker does not run because naphtha falls for one week.

It runs because the plan still holds together: feedstock arrives, the spread covers the run, and customers can take the molecules.

That is the issue now.

The weekly naphtha move is one input. It is not the decision.

Restart is not normalization

Lotte Chemical's Yeosu restart is a useful case study, but it should not be treated as broad operational relief.

OPIS / MarketWatch reported that Lotte Chemical restarted its Yeosu cracker in late May after a two-month maintenance period. Operating rates after restart were not confirmed.

A restart proves the asset can fire. It says much less about run rate, feedstock slate, margin cover, product outlets, or customer appetite.

Until those are visible, a restart belongs in the provisional-run bucket, not in a relief headline.

Japan is no longer just anecdotal

Reuters added a hard Japan data point on 29 May. Citing METI data, Reuters said Japan's April crude imports fell nearly 66% year-on-year to 850,000 b/d. Reuters reported this was the smallest volume since November 1962, based on past data viewable on Japan's National Diet Library website. Middle East imports fell 68%, domestic petrochemical-feedstock naphtha sales fell 35.6% to 406,231 b/d, and Japan and other Asian refiners deepened run cuts in April and May.

This does not mean every Japanese cracker is short.

It does mean the problem is visible in national energy data, not just in company anecdotes.

Reuters had already reported that Fumiya Kokubu, former Marubeni CEO, warned Japan could face chemical-product shortages from late June because replacing Middle Eastern naphtha is difficult.

The warning now has harder statistical backing.

Recovery signals do not close the file

There are also recovery signals.

Argus reported on 29 May that APIC delegates expect Japan's steam crackers to see a moderate recovery in run rates from June as alternative feedstock supplies improve. But the same report said poor margins and high feedstock prices may cap any production increase.

That does not weaken the run-plan question. It sharpens it.

A partial recovery still leaves the boardroom asking whether the asset clears on feedstock arrivals, spreads, co-product outlets, customer demand and cash, rather than on a single price print.

The structural file was already open

S&P Global's APIC 2026 material makes the point broader than Hormuz.

Asia's naphtha-fed cracker base was already under rationalization pressure before the latest feedstock shock. S&P says rationalization is expected to persist into 2027, with Japan leading planned capacity removals and South Korea targeting a 20%-28% reduction in ethylene capacity. S&P also says Japan's naphtha-fed steam crackers have been operating below full capacity since 2022 because of negative margins, with operating rates falling to 68.6% in March from 75.7% in February and 75.1% a year earlier.

Argus reported that Japan's average naphtha-fed ethylene cracker operating rate fell to 67.3% in April, a second consecutive record low, citing Japan Petrochemical Industry Association data.

The war shock did not create the weak asset base.

It exposed it.

Korea has moved into restructuring

Korea's policy signal is explicit.

Reuters reported that South Korea approved its first petrochemical restructuring project in February, involving HD Hyundai Oilbank, Lotte Chemical and HD Hyundai Chemical at Daesan. The approved project includes a temporary three-year shutdown of Lotte Chemical's Daesan naphtha cracking center.

That point matters because it separates confirmed action from broader expectation.

Only Daesan is confirmed in this file. Wider Korean capacity cuts remain a policy and industry target, not a published plant list.

This is why the question is moving beyond feedstock access. It now shapes which assets companies keep backing with cash, and which ones they start treating as candidates for review.

A ceasefire headline does not close the run-plan file

Reuters reported on 28 May that the United States and Iran had reached an agreement to extend their ceasefire and lift restrictions on shipping through the Strait of Hormuz, pending President Trump's approval. Iranian state media said the agreement had not been finalized.

A ceasefire headline can move sentiment.

It does not automatically validate a cracker run plan.

The run plan still depends on physical arrivals, insurance confidence, workable spreads and customer offtake.

What paid readers get

The paid layer is an Asia NCC operating screen for producers, procurement teams, traders, strategy teams and market-intelligence desks.

It does not predict named cracker shutdowns.

It helps a desk defend the weekly run plan using feedstock access, olefin spreads, merchant-cover economics, working capital, restart status and restructuring signals.

The free post explains why the weekly naphtha pullback is not enough.

The paid pack gives you the file you can walk into the run-plan meeting with.

Boardroom question

If you had to defend your current naphtha-cracker run plan tomorrow, would you show a file on feedstock arrivals, olefin spreads, merchant cover and cash, or just last week's naphtha price print?

Views expressed by independent contributors are their own and do not represent Matium.