Budapest, 30 June 2026

South Korea-linked resin pricing has moved from a policy headline into a negotiation issue.

The naphtha export restriction remains the legal reference point. MOTIR has not confirmed early abolition, and the official position still depends on Middle East conditions, Hormuz passage, and naphtha and petchem supply-demand.

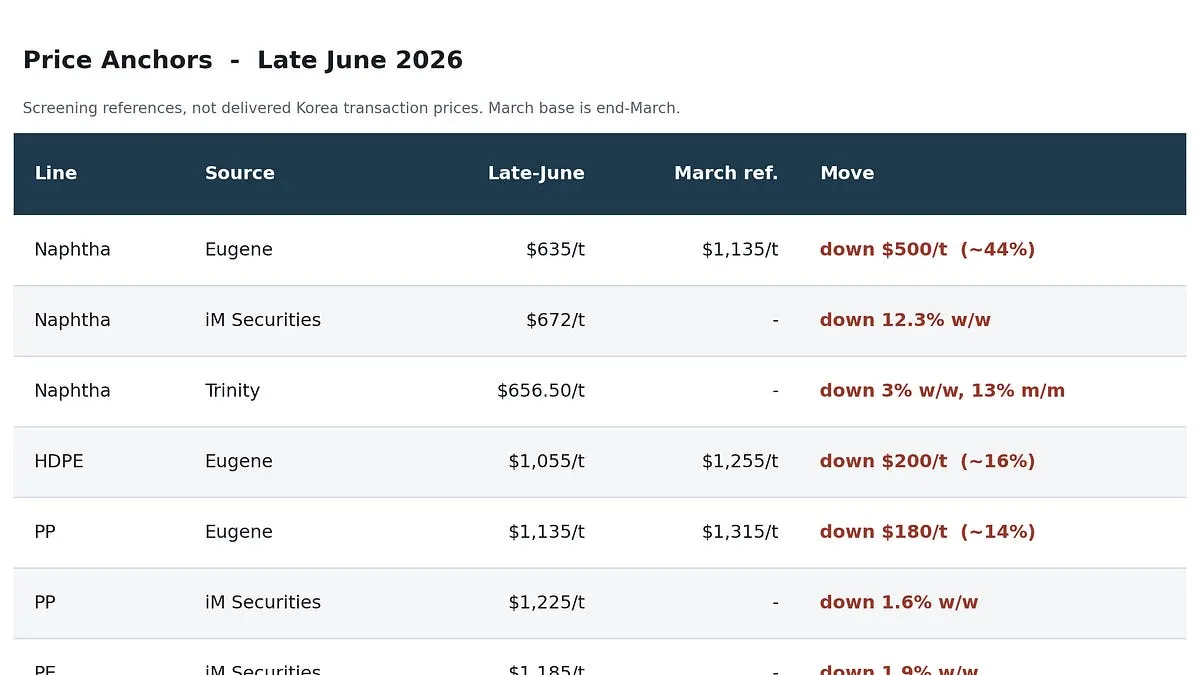

The operating picture has also changed. Korean reporting points to improved naphtha availability and higher cracker run rates. Crude procurement held up better than a pure disruption story would suggest. Late-June price references have moved away from the March stress window.

That creates a cleaner buyer question. A supplier can still point to the active rule, but a buyer can ask whether today's offer reflects current feedstock, resin replacement value, and spread logic.

LG Chem is the useful supplier-side marker. The company has announced targeted delivery-price support for selected SME customers using government naphtha support funds. That does not settle the wider market, though it changes the conversation with suppliers that still defend offers using March-May disruption language.

Procurement teams need the current basis. Distributors need to check inventory marks. Credit and LC desks need to look at collateral value and tenor.

Views expressed by independent contributors are their own and do not represent Matium.